12 May 3 Reasons Why You Should Not Be Worried About Apple’s 3Q Guidance

In Apple’s (NASDAQ: AAPL) 2Q2022 release, we saw Apple CEO Tim Cook giving guidance for 3Q2022 that didn’t make Wall Street very happy.

Cook revealed that supply chain constraints pertaining to COVID-driven plant shutdowns in the Shanghai area, along with industry component shortages, are expected to result in a substantial drag of US$4 billion to US$8 billion for fiscal 2022’s third quarter (3Q2022).

Also, with mounting inflationary pressures, Apple’s gross margin forecast of 42-43% implies that there may be a year on year margin contraction compared to the 43.3% in 3Q2021.

Investors of this blue-chip technology stock may wonder if this piece of news should get you worried.

But if you hold a long term view of the business, here are three reasons why you should not.

1. Demand for Apple’s products remains high

Remember that we are living in unusual times, with occurrences such asCOVID-19 and Russia’s invasion of Ukraine over the last two years.

These events have impacted companies large and small.

Yet, Apple was still able to pull in a strong set of results with revenue of US$97.2 billion, when analysts’ consensus was expecting US$94 billion.

Its diluted earnings per share of US$1.52 also beat analysts’ estimates of US$1.42.

Compared to 2Q2021, 2Q2022’s sales rose 9% or US$7.7 billion, driven primarily from the strong performance of its Services, iPhone and Mac product segments.

In 2Q22, Apple released the iPhone SE with 5G Technology, iPad Air and All-new Mac Studio (powered by the Apple M1, Max, Ultra chip) and All-new Apple Studio Display.

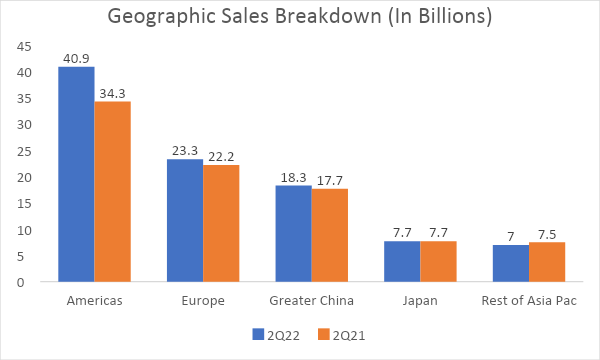

Source: Apple’s 10-Q SEC filings, segment information and geographic data

For investors watching China over the last few quarters, it is not surprising to see even big names affected by the lockdown and supply chain related issues.

It is interesting to note that despite the issues faced from lockdowns and component shortages, China still registered a 3.5% year on year growth for the quarter.

Growth in the Americas and Europe (68.3% of total revenue contribution) was driven mostly by higher net sales of iPhone, Services, and Mac.

This is not only a testament to Apple’s execution but also indicates how well these new rollouts have been received by consumers.

2. Services revenue growing fast

In the past, we’ve mentioned how Services revenue hit a quarterly record high of US$17.5b in 3Q2021 and that it’s a growing segment for Apple.

This was further seen in the 2Q2022 earnings breakdown below.

Services brought in US$19.8 billion of revenue, representing 20.4% of 2Q2022’s revenue.

Services revenue registered a growth of 17% compared to 2Q2021, and also represented the highest growth among all five of its segments.

|

|

Source: Apple 10-Q SEC filings, products and services performances

In tandem, it is also noteworthy to pay attention to how steadily Services Revenue has consistently grown over the last 3 years.

As of FY2021, Services Revenue has grown 47.7% compared to that of FY2019.

What this means is that Apple is successfully building its subscription base with services such as AppleCare, iCloud, payments, and advertising.

These services are becoming more meaningful contributors to Apple’s overall revenue pie and are closely linked to its whole ecosystem.

3. Ecosystem evolution as a strong moat

Apple’s influence on the market is significant as it is the largest contributor to the S&P 500 index.

Beyond the innovation driving the new staple Mac series, the iPad, and of course the iPhone, Apple has been extremely progressive and fervent in its other complementary business segments.

The Wearables, Home & Accessories business segment that covers iWatch, Airpods and HomePod, which has grown 12% in 2Q2022, was not something that was even around before 2014.

Apple’s strategy of enabling a seamless sync with its hardware (with backward compatibility), be it the iPhones, Macbooks or iPads made it difficult for consumers to switch over to its competitors.

Consumers rely very heavily on Apple’s ecosystem, and this is the key aspect that makes its competitive moat so powerful.

A quick example of how easy it is for Apple to start converting and monetising from multiple sources starts with the purchase of an iPhone.

The customer will then be offered an add-on of AppleCare (Services revenue).

From here, there’s a three-month free inclusion of Apple TV (Services revenue, too), which will spin off to a chargeable subscription like how you would pay for a Spotify (NYSE: SPOT) streaming music subscription.

This buffers the cycle of users who upgrade their hardware from Apple’s new launches yearly, and continuously brings in a user base that will grow in tandem with its ecosystem.

Investors may remain wary of how the stock may perform in the short-term as sentiment remains fragile for growth stocks.

However, Apple’s execution and ability to monetise from innovation-driven demand will continue to carry its business further in the long term.

Disclaimer: Kent Lee owns shares of Apple.